Plausible explanations exist for why low-volatility stocks perform better than their high-volatility counterparts.

In college finance courses, we are taught about the risk-return trade-off where expected return rises with increased risk. This insight is formalised in the Capital Asset Pricing Model (CAPM), which specifies the amount of compensation an investor needs for taking on additional risk.

Although the CAPM is a beautiful and elegant theory, there are many issues with its application in the real world. One fascinating anomaly Quants observe is that low-volatility, less risky stocks appear to outperform high-volatility stocks over the long term on a risk-adjusted basis.

Let’s replicate this anomaly ourselves in a backtest and discuss the results.

The methodology employed here is simple by design. The investment universe comprises all stocks in the FTSE World index from January 1994 to March 2016 (22 years and three months). At the start of every month, the volatility of every stock is calculated, where volatility is defined as the annualised standard deviation of the percentage price changes over the last 24 months. All stocks are then ranked from low to high volatility and split into deciles, with 10% of the market capitalisation of FTSE World in each decile. The returns of each decile over the month are then determined. This process is repeated at the start of every month and the return and volatility for each decile calculated for the entire period.

The striking results of the backtest are shown in Fig. 1. As we move from left to right, from the lower-volatility deciles to the higher-volatility deciles, the returns seem to decline. But what is particularly noticeable is the almost monotonic decrease in Sharpe ratios, a measure of excess return per unit of risk.

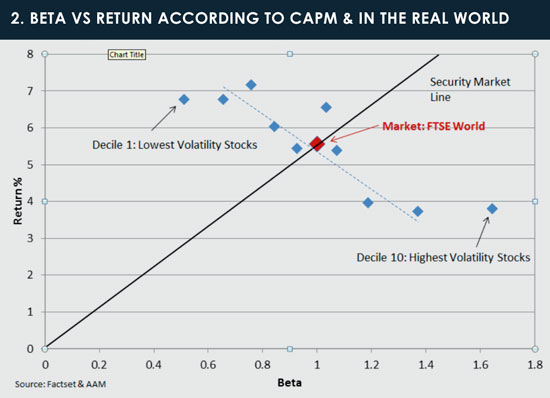

Another way of displaying the backtest results is to plot the return against beta (the volatility of the stock compared to the market) of each decile. If the CAPM held true, then all the deciles would lie close to the Security Market Line (SML), meaning excess return is a linear function of beta. Clearly this is not the case – if anything, the deciles seem to form a line perpendicular to the SML! Low-volatility stocks lie above the SML and hence have positive alpha, while high-volatility stocks have negative alpha.

Academics have shown that this anomaly goes back to 1963 in the US, and it occurs in both developed and emerging markets.

Explanations for low-volatility outperformance

There are several plausible explanations for this anomaly.

One rationale might be due to fund manager compensation where the manager is paid a bonus if performance is sufficiently high. More volatile portfolios increase the expected value of the bonus.

Another explanation is that fund managers favour newsworthy stocks, for which they can make a compelling investment case. But because of the relatively intense newsflow surrounding these stocks, their returns are often volatile. Baker & Haugen (2012) say agency issues such as the two just described create excess demand for highly volatile stocks, which boost prices and depress future expected returns.

Another explanation is that fund managers favour newsworthy stocks, for which they can make a compelling investment case. But because of the relatively intense newsflow surrounding these stocks, their returns are often volatile. Baker & Haugen (2012) say agency issues such as the two just described create excess demand for highly volatile stocks, which boost prices and depress future expected returns.

A recent paper by academics at the London School of Economics suggests the anomaly could be related to the so-called ‘Curse of the Benchmark’. If the price of a stock doubles and a manager has a half-weight relative to the benchmark, then the active bet doubles. On the other hand, if the price halves, then the negative active bet halves also. Hence volatile stocks have the greatest potential to cause underperformance, meaning managers have an incentive to buy such stocks and neutralise positions relative to their benchmark.

Whatever the true explanation for this observed anomaly, the simple backtest described above provides powerful empirical evidence of the risk-adjusted outperformance of low-volatility stocks.

References

Ang, Andrew (2014) ‘Asset Management’, Oxford University Press; Baker, Nardin & Haugen, Robert (2012) ‘Low Risk Stocks Outperform within All Observable Markets of the World’, LowVolatilityStocks.com; Blitz, David & van Vliet, Pim (2007) ‘The volatility effect: lower risk without lower return’, Robeco Asset Management; Vayanos, Dimitri & Woolley, Paul (2016) ‘Curse of the Benchmarks’, London School of Economics

Disclaimer: For professional investors only – not for use by retail investors.

Aberdeen Asset Middle East Limited (“AAMEL”) registered in the Abu Dhabi Global Market (“ADGM”) (Registered No. 000000252) is regulated by the Financial Services Regulatory Authority (“FSRA”). This is not investment research as defined by the FSRA. The information is not intended to lead to the conclusion of a contract of any nature what so ever within the territory of the ADGM. The recipient of the information understands, acknowledges and agrees that the contents of this document have not been approved by the FSRA or any other regulatory body or authority in the United Arab Emirates. By accepting to receive this document, you represent that you are a’ Market Counterparty’ or a ‘Professional Client’ and you agree to be bound by the foregoing limitations.

This document is for information purposes only. Nothing contained in this report is intended to constitute ‘Advising on Financial Products or Credit’ or ‘Arranging Credit or Deals in Investments’ as defined by the FSRA. This document does not constitute or form part of any marketing initiative, any offer to issue or sell, or any solicitation of any offer to subscribe or purchase, any products, strategies or other services nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract resulting therefrom. In the event that the recipient of this document wishes to receive further information with regard to any products, strategies other services, it shall specifically request the same in writing from us.

The value of investments and the income from them can go down as well as up and investors may get back less than the amount invested. Past performance is not a guide to future results.

©2017 funds global mena