![]()

Lloyd George Management (LGM) believes frontier markets offer compelling prospective long-term returns. Sophisticated investors seeking the next emergent asset class may find frontier markets to be a long-term option as part of diversified portfolios.

THE NEXT EMERGING MARKETS

In 1990, emerging markets were often considered risky investments and constituted, at most, a marginal weighting in investors’ portfolios. They are now prime drivers of global economic growth and have achieved recognition as a well-established asset class.

Today, while the long-term fundamental picture for emerging markets remains attractive, the opportunity for significant alpha generation has expanded to encompass previously more obscure countries across Africa, Eastern Europe, the Balkans, Baltic States, Middle East, Latin America, the Caribbean and Asia. As a group, these countries have become known as the “frontier markets”.

Frontier market countries tend to have market-orientated economies in the early stages of development and are widely regarded as the natural successors to the initial group of emerging markets.

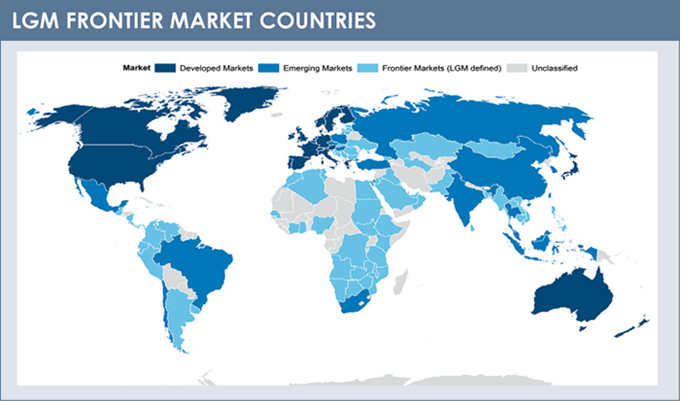

The following map outlines LGM’s frontier market universe. In addition to the 26 MSCI Frontier Markets Index countries, it includes four smaller emerging market countries and countries excluded from frontier indices for reasons including low liquidity or a scarcity of investible companies, but which may present attractive individual investment opportunities. Several factors suggest that frontier markets represent fertile ground for the next generation of attractive long-term investment returns.

ECONOMIC STRENGTH

The IMF’s five year growth rate forecast for frontier economies of 5.3% pa compares favourably with the forecast of 2.9% pa for developed economies (2010 – 2016 CAGR, Source: IMF, (LGM Frontier Markets Universe). The absence of the extreme levels of indebtedness with which developed nations are currently burdened is a strong positive for frontier countries at the macro, corporate and household levels.

While individual countries’ potential varies significantly, frontier markets collectively offer strong GDP growth prospects; an abundance of natural resources (including around 45% of global oil reserves and 25% of arable land. Source: IMF, World Bank, UN FAOSTAT, LGM Frontier Markets Universe); and demographic advantages including young, growing populations. Strikingly, while the UN population division predicts that the ratio of working age population to dependent population will worsen for emerging markets from 2017, the picture will continue to improve for frontier countries until 2045.

While individual countries’ potential varies significantly, frontier markets collectively offer strong GDP growth prospects; an abundance of natural resources (including around 45% of global oil reserves and 25% of arable land. Source: IMF, World Bank, UN FAOSTAT, LGM Frontier Markets Universe); and demographic advantages including young, growing populations. Strikingly, while the UN population division predicts that the ratio of working age population to dependent population will worsen for emerging markets from 2017, the picture will continue to improve for frontier countries until 2045.

SUBSTANTIAL RISK DIVERSIFICATION

Positive drivers relating to equity markets include: the prospect for expansion and liberalisation of frontier stock markets; diversification benefits; stock market inefficiencies that create alpha-generation opportunities; and attractive equity valuations and dividend yields.

Despite equity market correlations recently rising, the diversification benefit offered by an allocation to frontier markets remains substantial.

ATTRACTIVE VALUATIONS AND DIVIDEND YIELDS

Frontier market equity valuations look reasonably attractive relative to both emerging and developed counterparts, and their own history. On a forward P/E basis, frontier stocks trade broadly in line with emerging markets, but if one considers the substantially larger dividend yield offered by frontier stocks (4.0% vs. 2.6% for emerging markets), the case for frontier remains compelling.

DEDICATED TEAM

LGM’s dedicated Frontier Markets London-based investment team is led by Thomas Vester, CFA, who managed Frontier Market portfolios at BankInvest in Copenhagen for around 4 years from September 2007. Thomas is supported by two experienced frontier Analysts and specialist Advisors, including Dr Greg Mills, head of Johannesburg-based Brenthurst Foundation.

Inefficiencies also permeate the market trading environment where volumes can be thin and, consequently, bid-ask spreads are often large. Trading is a very specific skill in frontier markets. Local connections and deep market knowledge help provide LGM with a further edge.

BENCHMARK REFLECTS LONG-TERM OBJECTIVE

In order to offer clients a balance of attractive opportunities across the range of frontier countries, LGM believes a blended index of 50% MSCI Frontier Markets Index and 50% MSCI Frontier Markets (ex-GCC) Index is appropriate.

This composite benchmark mitigates against the heavy GCC concentration of the MSCI Frontier Markets Index, which LGM considers to be subject to economic factors which may not reflect its long-term objective to capture growth from the rising income levels of the frontier markets’ consumer.

LGM’S FOCUSED INVESTMENT APPROACH

LGM’s investment philosophy is predicated on the view that financial markets are inefficient and pricing anomalies may persist for prolonged periods, particularly in frontier markets.

In the long-term, the firm believes market pricing will reflect corporate fundamentals, and reward companies with structurally-attractive business models stewarded by skilful, prudent management teams

that apply strong capital discipline to generate cash returns above cost of capital across the business cycle.

The team aims to exploit these inefficiencies with its long-term fundamental investment approach, which is primarily focused on intensive company research. This is complemented by a macroeconomic framework which helps set the context for company analysis and maximises research effort quality by identifying countries and sectors on which to focus and, in some cases, avoid.

Full assessment of a company requires first hand meetings with management, often over several years. Regular visits to frontier countries are essential to understand dynamics, not only of the corporate sector but also of the local financial and macroeconomic environment.

The team emphasises the importance of primary research; in 2012 they conducted more than 280 meetings, and met with companies in 23 countries. The importance of such meetings can hardly be overstated, given a lack of consistently-presented accounting information and other information sources.

These inefficiencies do, however, offer the opportunity to buy attractively-mispriced investments, for those willing to conduct their own due diligence.

LGM’s objective is to build a non-benchmark driven portfolio of 30-60 holdings with considerable outperformance potential. They aim for low turnover, typically anticipating at least a five-year holding period and to add alpha across the market cycle.

For further information, please contact Firas Mallah, Managing Director, BMO GAM Abu Dhabi at [email protected], +97126594254 or visit bmo.com/lloydgeorge.

Disclaimer: This document has been prepared and issued by Lloyd George Management (Europe) Limited (authorised and regulated in the UK by the Financial Conduct Authority). Lloyd George Management (Europe) Limited is incorporated in England and Wales under Registered Number 3029249 and has its registered office at 78 Brook Street, London W1K 5EF. Any reference to Lloyd George Management or LGM in this document encompasses all subsidiary companies of LGM (Bermuda) Limited, a wholly-owned subsidiary of Bank of Montreal (BMO).

This is not intended to serve as a complete analysis of every material fact regarding any company, industry or security. The opinions expressed here reflect our judgment at this date and are subject to change. Information has been obtained from sources considered reliable, but accuracy cannot be guaranteed. This publication is prepared for general information only and does not constitute investment advice and is not intended as an endorsement of any specific investment. It does not have regard to the specific investment objectives, financial situation and particular needs of any specific person who may receive this report. Investors should seek advice regarding the appropriateness of investing in any investment strategy discussed or recommended in this report and understand that statements regarding future prospects may not be realised. Investment involves risk. Market conditions and trends will fluctuate. The value of an investment as well as associated income may rise or fall. Accordingly, investors may receive less than originally invested.

The material in this publication has been prepared solely for distribution to professional and qualified investors.